The Tokyo Seimitsu Group conducts its semiconductor manufacturing equipment and precision measuring instrument businesses globally. As such, we are committed to developing leading-edge products and elemental technologies that cover advanced needs of our customers, despite the challenges of demand fluctuations, as well as macroeconomic and geopolitical risks. As CFO, I believe it is important to strike a balance between making decisions on investments in tangible and intangible assets required for our future growth and boosting corporate value, and returning profits to our shareholders, employees, and suppliers, all while maintaining the stability of our financial base.

We are facing what is called a new normal across so many areas these days, particularly with our post-COVID-19 lifestyles, our approach to work, and weather events. The business environment is also undergoing reform toward a new normal—increases in the prices of commodities and interest rates, sudden fluctuations in exchange rates, the rapid spread of generative AI, the shift to New Energy Vehicles (NEVs) and fast development of autonomous driving, digitalization and proliferation of DX. I feel that these will call for a response covering a broader scope than ever before.

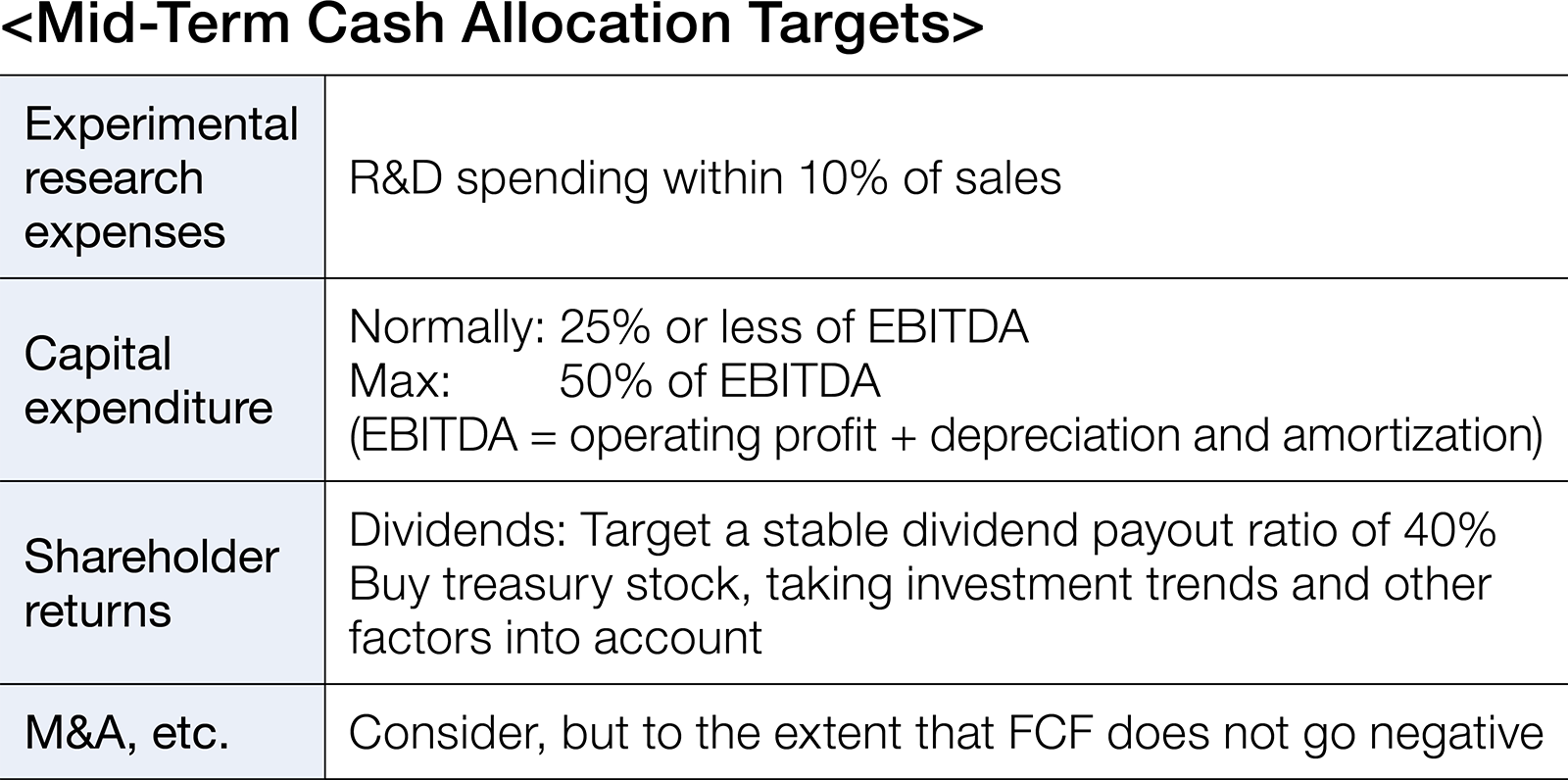

The industry in which the Tokyo Seimitsu Group operates requires us to maintain our technological superiority through research and development and to anticipate the needs of our leading-edge customers. Accordingly, we regularly review R&D expenditures and the profit/loss of each product business, taking into account future demand forecasts and customer trends. From the results of reviews, we will make the decision to withdraw from product businesses that have no potential improvement in profitability within a certain period of time. As an indicator for research and development, we aim to keep R&D expenses around 10% of net sales.

In addition, beginning with the current mid-term business plan, we apply ROIC as an internal evaluation method, and use this metric to determine whether the return generated from investment into each business unit is commensurate with investment costs, and make use of it in management, including for making investment decisions. We developed the framework required for these calculations and management in fiscal 2022, and began reviewing the results of ROIC.

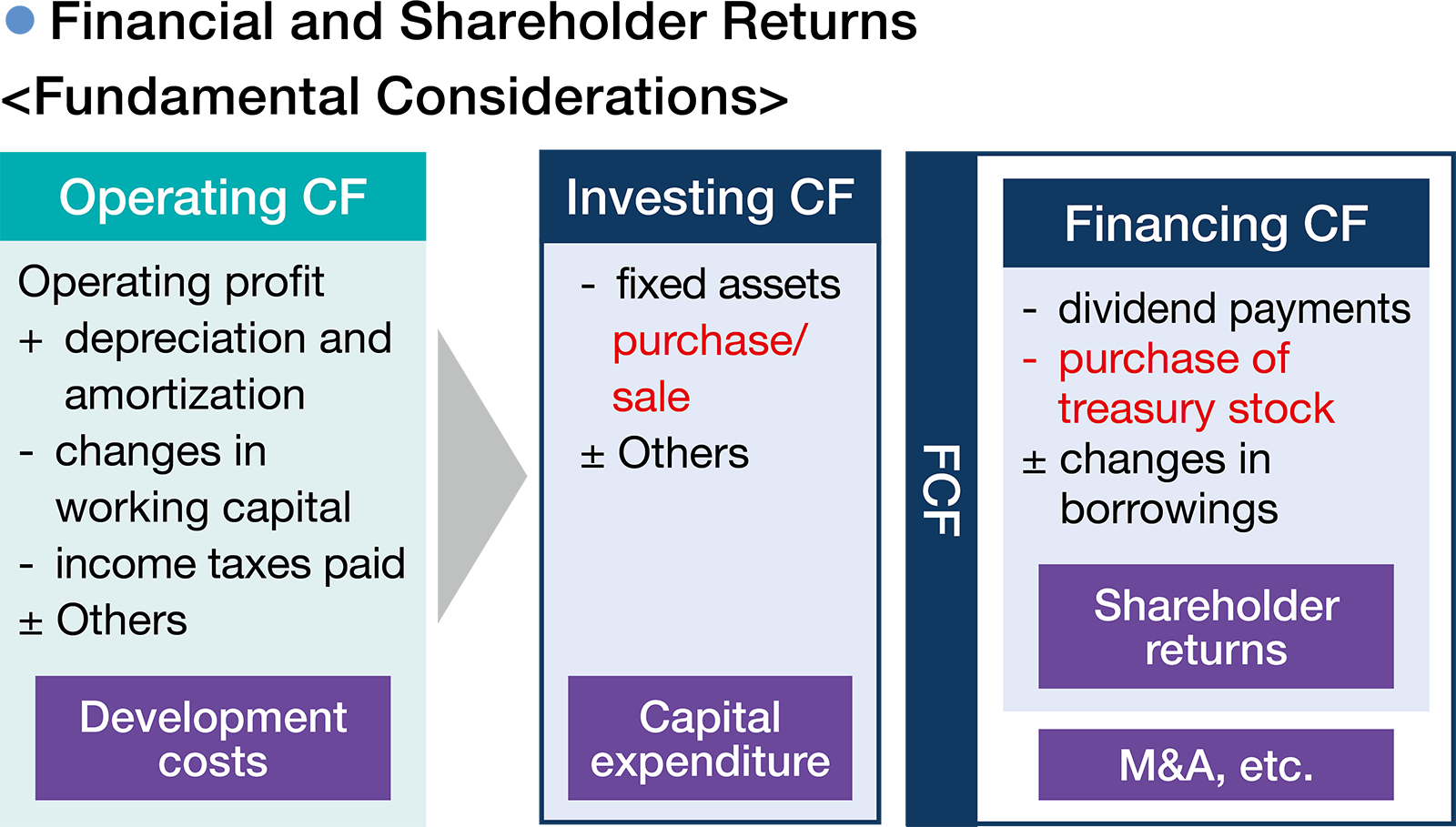

We maintain capital investments at around 25% of EBITDA (operating profit before depreciation) normally, with 50% of EBITDA as our maximum level. We are making the expansion of production capacity an urgent priority, particularly in the semiconductor manufacturing equipment business, where long-term market growth is expected. The Hanno Plant (in Hanno City, Saitama Prefecture) began operations in July 2023, and we began studies for the construction of a plant in the Nagoya region to begin operating from 2025.

We also consider M&A to be an effective means of achieving growth by utilizing retained earnings and are considering making acquisitions within the scope of our free cash flow.

To strengthen our relationship with stakeholders like subcontracting vendors who have been vital for the growth of the Company, we are working on shortening the terms of payment for accounts payable.

Tokyo Seimitsu considers the consistent return of profits to shareholders to be one of its most important management tasks. From this perspective, we will use a system of paying dividends in accordance with profit distribution, with 40% as our target consolidated dividend payout ratio. The Company regards share buyback as a flexible profit return that complements the payment of dividends from retained earnings, while comprehensively taking into account cash flow, retained earnings, and other factors.

The Tokyo Seimitsu Group’s industry is subject to significant market volatility. Accordingly, we believe it is important to maintain a certain level of cash, deposits, and equity to absorb the impact of market fluctuations. We manage cash and deposits based on cash flow trends, including investment projects, and take into overall consideration of the balance with investor returns.

Cash dividends per share for fiscal 2023 was 235 yen, with a dividend payout ratio of 40.3%. We are also purchasing 2.5 billion yen of treasury stock through to the next fiscal year.

With the drastic changes occurring throughout society as a whole, semiconductors continue to play a greater role in so many areas, and measuring instruments remain essential throughout the manufacturing sector—significant growth is anticipated in both of these industries. The semiconductor industry in particular has become the focus of national policies in many countries around the world, which are boosting investment into the sector. This is a field in which significant growth is anticipated, but there are also concerns over risks potentially caused by unexpected situations.

Given these circumstances, as the CFO, it is my mission to ensure the Company survives in the face of global economic uncertainty and to maintain our financial condition to facilitate smooth investments that contribute to growth. As a result, we will continue to provide products that make full use of cutting- edge technologies, and thereby boost our corporate value.